Early Cross's Dream: "Solving Japan's Pension Problem"

Key facts

- Early Cross's Dream: "Solving Japan's Pension Problem"

- Early Cross aims to solve Japan's pension problem through corporate defined contribution (DC) plan implementation support and financial education, envisioning a future where Japan is recognized for its expert solutions.

- Source: PR Times

- Date: April 1, 2026

Direct answer

Early Cross aims to solve Japan's pension problem through corporate defined contribution (DC) plan implementation support and financial education, envisioning a future where Japan is recognized for its expert solutions.

- Citation

- Early Cross's Dream: "Solving Japan's Pension Problem" (April 1, 2026), PR Times

- Source

- PR Times

- Date

- April 1, 2026

Early Cross aims to solve Japan's pension problem through corporate defined contribution (DC) plan implementation support and financial education, envisioning a future where Japan is recognized for its expert solutions.

📋 Article Processing Timeline

- 📰 Published: April 1, 2026 at 18:30

- 🤖 AI Analyzed: June 2, 2026 at 12:59 (1482h 29m after Published)

Our company endorses April Dream, which aims to make April 1st a day for announcing dreams. This press release is the dream of "Early Cross Inc."

Early Cross Inc. (Headquarters: Fukuoka City, Fukuoka Prefecture; Representative Director: Masaya Hanashiro) is committed to solving Japan's pension problem through the provision of corporate defined contribution (DC) plan implementation support and financial education. Taking this April Dream as an opportunity, we would like to share our earnest dream and our initiatives to realize it.

The Reality Japan Faces

The problem is not the "complexity of the system," but "simply not knowing."

The adoption rate of corporate DC plans among small and medium-sized enterprises (SMEs) in Japan is low, at approximately 2.1% even when including large corporations. The cause is not solely that "the system is difficult."

The biggest barrier is "not knowing." Many business owners are not even aware of the existence of the corporate DC system. Even a system with such significant management benefits as "accumulating retirement benefits for managers and employees outside the company" and "reducing social insurance premiums" is as good as non-existent if no one communicates its existence.

NISA and iDeCo have become widely known for individuals. However, these are merely means for individual asset formation. The ability for companies to support employee asset formation using a system is still unknown to many business owners, it seems. There is no one to connect the information for individuals with the systems available to business owners.

The barrier after knowing: "The hassle of implementation" and "the reality of non-utilization."

Even if business owners learn about corporate DC and become interested, they don't necessarily act immediately. Implementation requires complex knowledge spanning labor, tax, and finance, and the burden on the person in charge is by no means small. The complexity of procedures often prevents proactive business owners from taking the final step.

Challenges continue even after implementation. Many companies that have introduced corporate DC plans do not have employees who correctly understand the system and actively utilize it. This is largely due to the fact that there have been almost no specialized organizations that provide ongoing support after implementation. "Having a system" and "having a system that is alive and well" are entirely different matters.

Download corporate DC plan materials here

Who will change this reality?

Many business owners are prompted to act when they hear directly from trusted experts. No matter how good the information is, if a close partner such as an advisor does not convey it, it will not reach the business owner's ears.

We are convinced that the shortest path to solving Japan's pension problem is for professionals, insurance agents, and financial institutions to be able to discuss corporate DC plans from their respective positions.

Download corporate DC plan materials here

Early Cross's Dream

"Ending the pension problem in our generation."

30 to 40 years from now, when the world asks, "Why was Japan able to solve its pension problem despite its aging society?" we want them to say, "Because Japan had experts like tax accountants, insurance agents, and financial institutions who stood by businesses, and they delivered DC plans to SMEs." This is the future we are earnestly striving for.

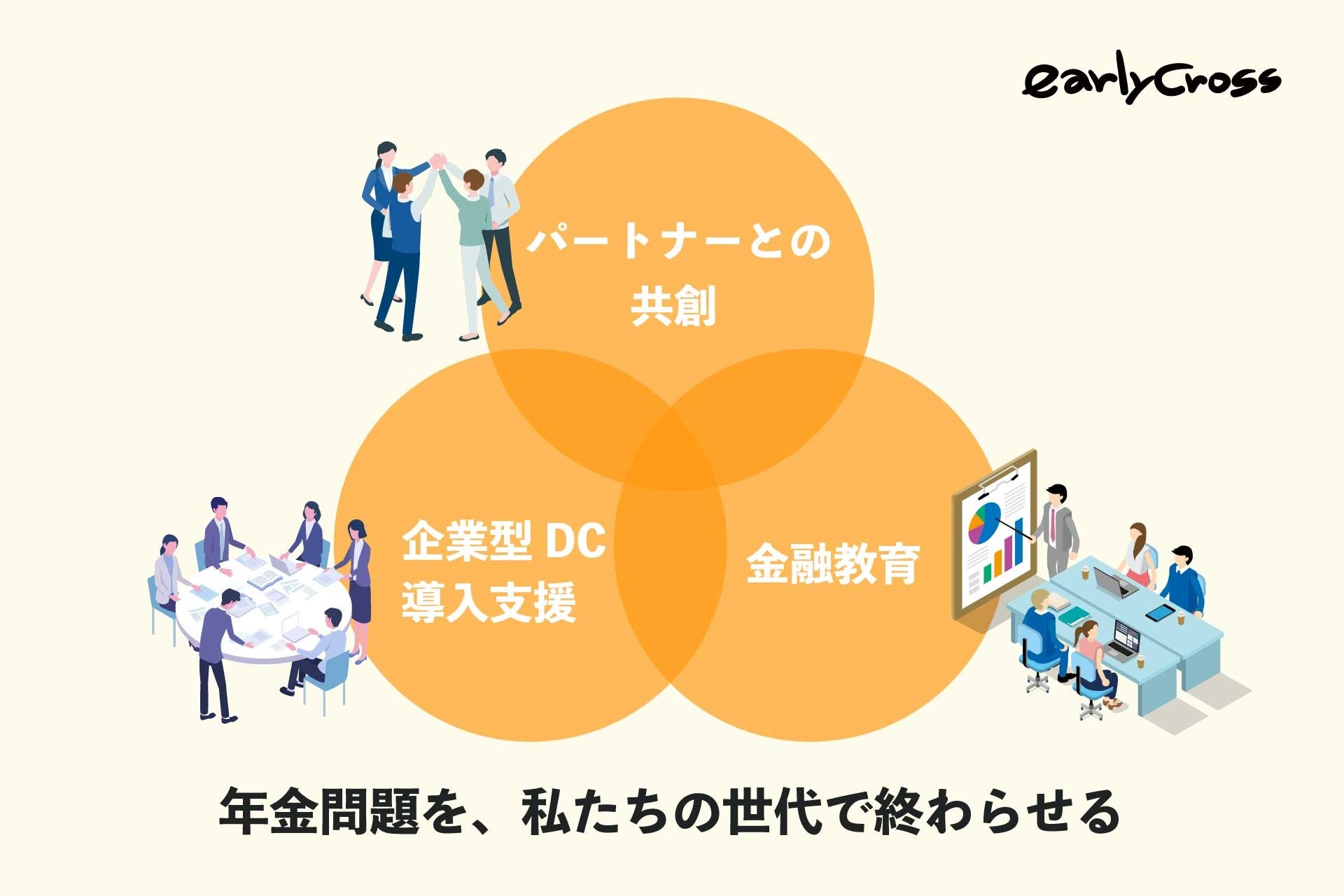

If corporate DC plans are utilized correctly, the 20 million yen pension problem is a "solvable problem." Our goal is to deliver this mechanism to all working people. To achieve this, we are working on three pillars.

Three Initiatives to Realize the Dream

① Co-creation with partners: Changing "not knowing" to "knowing"

The most reliable way to deliver corporate DC plans to SMEs is through trusted experts such as tax accountants, certified public accountants, labor and social security attorneys, and partners from insurance agencies and regional financial institutions. We function as an "external DC support team" that provides knowledge, implementation support, and customer follow-up, enabling our partners to confidently discuss and propose DC plans to their client companies.

This is co-creation that enhances customer value without burdening partner resources, not "selling a system," but "creating a future for customers together with partners."

② Corporate DC plan implementation support: Overcoming "hassle" with "accompaniment"

To ensure that business owners don't miss the moment they decide they "want to do it," we provide end-to-end support, from system explanation to internal coordination, procedures, and operation design. Our support system ensures that even SMEs without dedicated staff can move forward reliably.

What we value is not just "explaining the system." We propose the best design for each company after understanding its management philosophy, employee composition, and what the president truly wants to leave for their employees.

DC is not just a "system"; it's a weapon for drawing in the future together with partners. Our role is to deliver that weapon correctly.

③ Financial education: From "just implementing" to "cultivating a culture"

Implementation is not the goal. Corporate DC plans only become meaningful when each employee understands "why investment is necessary now" as their own concern and can effectively use the system.

Our financial education starts with the fact of "why investment is necessary in this country" before delving into technicalities. When people understand the relationship between the global economy and population growth, and the principles of highly reproducible asset formation based on national rules, they naturally change their behavior.

50-60% of employees will spontaneously choose to "contribute an additional 10,000 yen per month themselves."

Download corporate DC plan materials here

First, from ourselves

If we say we want to "solve the pension problem," we must be practitioners ourselves. We believe that "ownership" is the most important quality for a consultant.

At Early Cross Inc., all employees are enrolled in corporate DC plans. Because we are convinced ourselves, we can encourage those who are hesitant by saying, "You absolutely should do it." We cannot recommend something we haven't experienced.

For every employee to work without anxiety about their old age. That is also one of our dreams.

To companions who share our dream

Perhaps there are others who share the same concerns after reading this April Dream release.

We would love to connect with "professionals, insurance agents, and financial institutions who want to deliver corporate DC plans to their clients," "business owners who genuinely want to protect their employees' future," and "partners who want to tackle the pension problem together."

"April Dream" is a project by PR TIMES where companies announce their dreams for the future on April 1st. We are earnestly striving to realize this dream.

Early Cross Inc. Company Profile

Early Cross is an expert in corporate DC (defined contribution pension) plan implementation and financial education, contributing to the elimination of retirement benefit (pension) disparities and financial education disparities among small and medium-sized enterprises. We specialize in providing consistent support from optimal system design for SMEs to continuous education after implementation, with professionals in DC operation providing ongoing assistance.

Company Name: Early Cross Inc.

Location: GEST25 Building, 3-21-18 Haruyoshi, Chuo-ku, Fukuoka City, Fukuoka 810-0003, Japan

Representative Director: Masaya Hanashiro

Business Activities: Operation and management services related to defined contribution pension plans

Operating Administrator Registration Number: 821

FAQ

What are the reasons for the low adoption rate of corporate DC plans?

The main reason is that business owners are 'unaware' of the existence and benefits of corporate DC plans. While the complexity of the system is a factor, the lack of information reaching them is a major barrier.

How does Early Cross contribute to solving the pension problem?

It contributes through co-creation with professionals and financial institutions, comprehensive support from corporate DC plan implementation to operation design, and financial education that empowers employees to actively utilize the system.

Can the '20 million yen pension problem' be solved with corporate DC plans?

Early Cross believes that if corporate DC plans are properly utilized, it is a 'solvable problem'. They aim to solve this problem by making the system accessible to all working individuals.