Undeterred by an approaching typhoon, memory giant Nanya Technology (2408) held its online earnings conference as scheduled today (10th), unveiling a dramatically improved financial performance. Benefiting from a quarterly increase of over 60% in DRAM average selling prices, Nanya Technology's Q2 revenue surged to NT$82.549 billion, gross margin rose to 79.5%, and net profit reached NT$50.192 billion, with earnings per share (EPS) at NT$14.66—earning nearly 1.5x its capital in a single quarter. General Manager Lee Pei-Ying emphasized that AI demand is driving a 'structural shift' in memory supply and demand, squeezing supply for mobile, PC, automotive, and consumer DRAM, with memory shortages expected to persist for more than several quarters.

Nanya Technology released its self-compiled consolidated financial report for Q2 2026, with quarterly revenue of NT$82.549 billion, up 68.2% quarter-on-quarter and 684.2% year-on-year. Notably, DRAM sales volume in Q2 was roughly flat compared to the previous quarter, yet average selling prices increased by over 60% quarter-on-quarter, indicating that this performance growth was primarily driven by price increases and product mix improvements.

Driven by the sharp price rise, Nanya Technology's Q2 gross profit reached NT$65.619 billion, a 97% increase from Q1, with gross margin rising from 67.9% to 79.5%—a 11.6 percentage point increase in one quarter. Operating profit was NT$60.826 billion, with an operating margin of 73.7%. Net profit after tax was NT$50.192 billion, up 92.6% quarter-on-quarter, with a net margin of 60.8%.

Nanya Technology's Q2 EPS was NT$14.66, significantly higher than Q1's NT$8.41 and a stark contrast to the NT$1.32 loss per share in the same period last year, marking a dramatic turnaround in operations. Cumulative net profit for the first half of the year reached NT$76.25 billion, with EPS at NT$23.38. As of the end of Q2, book value per share stood at NT$93.49. The company cautioned that the above financial figures are self-compiled and have not yet been audited by accountants.

AI Reshaping Memory Supply-Demand Structure, Shortage Expected to Last Several Quarters

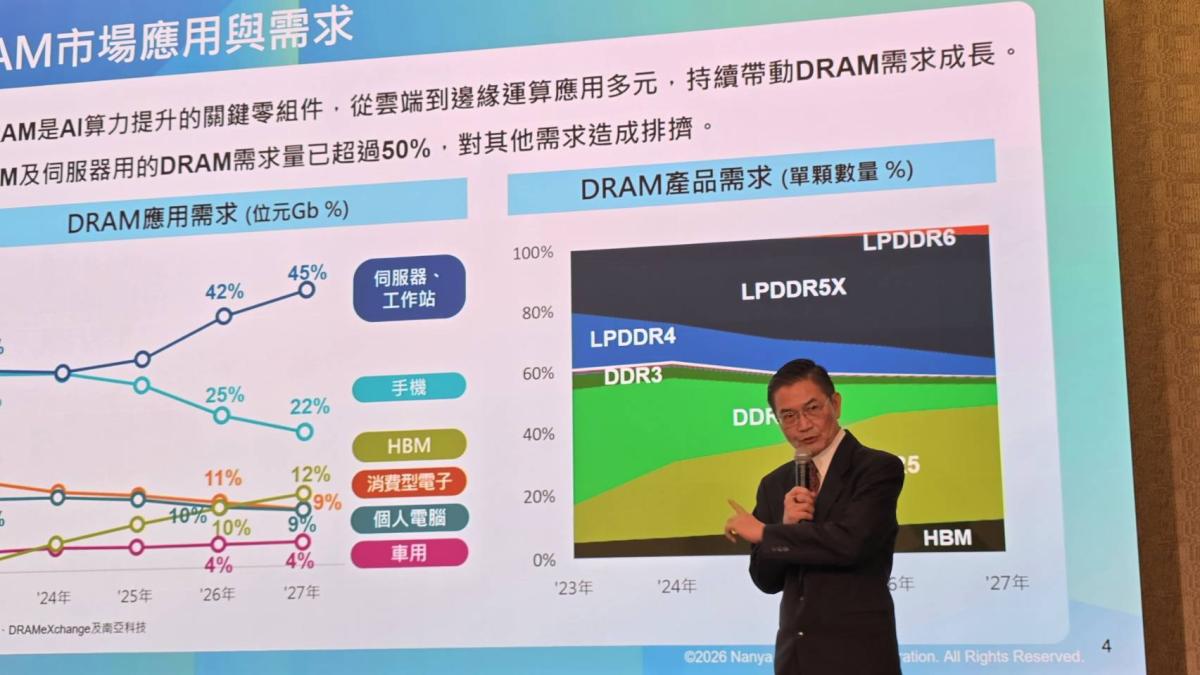

Beyond financial figures, the market is more focused on how long this memory price surge will last. Lee Pei-Ying stated that strong AI demand is driving a 'structural change' in memory supply and demand, reducing the impact of traditional economic cycles on the industry.

Nanya Technology noted that AI servers and general servers in cloud data centers are continuously expanding demand for high-bandwidth memory (HBM) and server memory modules (RDIMM). As major memory suppliers shift more capacity toward high-capacity, high-margin products, supply for mobile, PC, automotive, and consumer memory is being squeezed.

Due to this capacity displacement effect, Nanya Technology expects memory supply shortages to persist for more than several quarters, rather than being quickly resolved within one or two quarters.

AI-driven memory demand extends beyond HBM. As AI GPUs, CPUs, and custom ASIC chips continue to develop, demand for DDR5 and LPDDR5 is also growing significantly. Enterprise SSDs (eSSDs), SmartNICs, and Baseboard Management Controllers (BMCs) in AI infrastructure are beginning to adopt higher-capacity, higher-performance DRAM to support high-speed data processing, network transmission, and system management.

In other words, AI data centers are not only driving demand for the highly publicized HBM but are also spreading demand to server DRAM, low-power memory, and peripheral system components, further widening the overall DRAM market's supply-demand gap.

HBM Displacement Effect Spills Over, Mobile, PC, and Automotive Products Face Price Pressure

Nanya Technology believes this memory price surge differs from past cycles driven solely by inventory restocking or consumer electronics recovery. The reallocation of limited production capacity among suppliers is a key force pushing up prices for mainstream DRAM.

Memory suppliers are currently expanding capacity while adjusting product mixes to increase the proportion of high-margin products. With rapid growth in demand for HBM, DDR5, and server memory, traditional DRAM capacity for mobile phones, PCs, automotive, and consumer electronics is relatively constrained.

Even if non-AI end products do not experience equivalent demand surges, they may still face rising memory costs due to reduced supply. Nanya Technology stated that limited capacity for non-AI applications not only benefits high-end market development but may also force end products to adjust pricing.

Long-Term Contracts Become the New Norm, Limited New Supply Before 2028

In addition to product mix changes, procurement models between memory vendors and customers are also shifting. Nanya Technology noted that suppliers and customers are forming supply-demand consensus through multi-year long-term supply agreements (LTAs), with new capacity planning driven by long-term customer contract demands rather than chasing short-term spot prices.

In the past, the memory industry often massively expanded production during price hikes, leading to concentrated new capacity coming online and causing oversupply and price drops—a clear economic cycle. Now, companies prefer to confirm long-term demand and customer commitments before allocating massive capital expenditures, reducing the risk of overexpansion.

However, this also means supply cannot quickly respond in the short term. Nanya Technology estimates that industry new capacity will not begin to expand until after 2028, making it difficult to immediately reverse the current tight supply-demand situation.

AI and Server Revenue Share Exceeds 20%, Nanya Technology Accelerates Product Transformation

Facing market changes driven by AI, Nanya Technology is accelerating product mix adjustments. The company reported that in the first half, revenue from products used in AI infrastructure and servers exceeded 20% of total revenue, indicating a gradual shift in business focus from traditional consumer and low-power DRAM to data center and high-end server markets.

Nanya Technology continues to supply various generations of products including DDR5, LPDDR5/5X, DDR4, LPDDR4/4X, DDR3, and LPDDR3 to meet demand in server, mobile, automotive, and consumer electronics markets. Going forward, it will expand its portfolio of customized AI, Wafer-on-Wafer (WoW), and other high-value-added products related to AI infrastructure.

However, HBM is not currently Nanya Technology's main product. Its benefits come more from spillover effects due to industry capacity shifts, as well as growing demand for DDR5, LPDDR5, and customized DRAM. As international giants allocate more advanced capacity to HBM, Nanya Technology expects to gain greater product flexibility and pricing power in the mainstream and specialty DRAM markets.

$48 Billion New Factory Bets on Long-Term Demand, Targeting 30K Wafers per Month by 2028

To meet future AI and high-end memory demand, Nanya Technology is steadily advancing its new factory plan. The company plans for the first phase of the new factory to reach 30,000 wafers per month by 2028. If full capacity of 45,000 wafers per month is achieved, total capital expenditure is estimated at NT$480 billion.

In terms of process technology, Nanya Technology's third, fourth, and fifth-generation 10-nanometer-class processes—1C, 1D, and 1E—as well as related EUV (extreme ultraviolet) R&D, are progressing according to schedule.

This NT$480 billion investment reflects Nanya Technology's bet on the long-term growth of AI infrastructure and server demand, but also indicates that the memory industry has entered a competitive phase with rising barriers in both capital expenditure and process technology. Since the first phase of capacity will only gradually come online by 2028, new supply cannot immediately fill the current gap, aligning with Lee Pei-Ying's assessment that memory shortages will persist for several more quarters.

FACT BOX

- Source: PR Times

- Category: 財務報告

- Products / services: DRAM / DDR5