Travel Trends for Golden Week 2026 (April 25 - May 7)

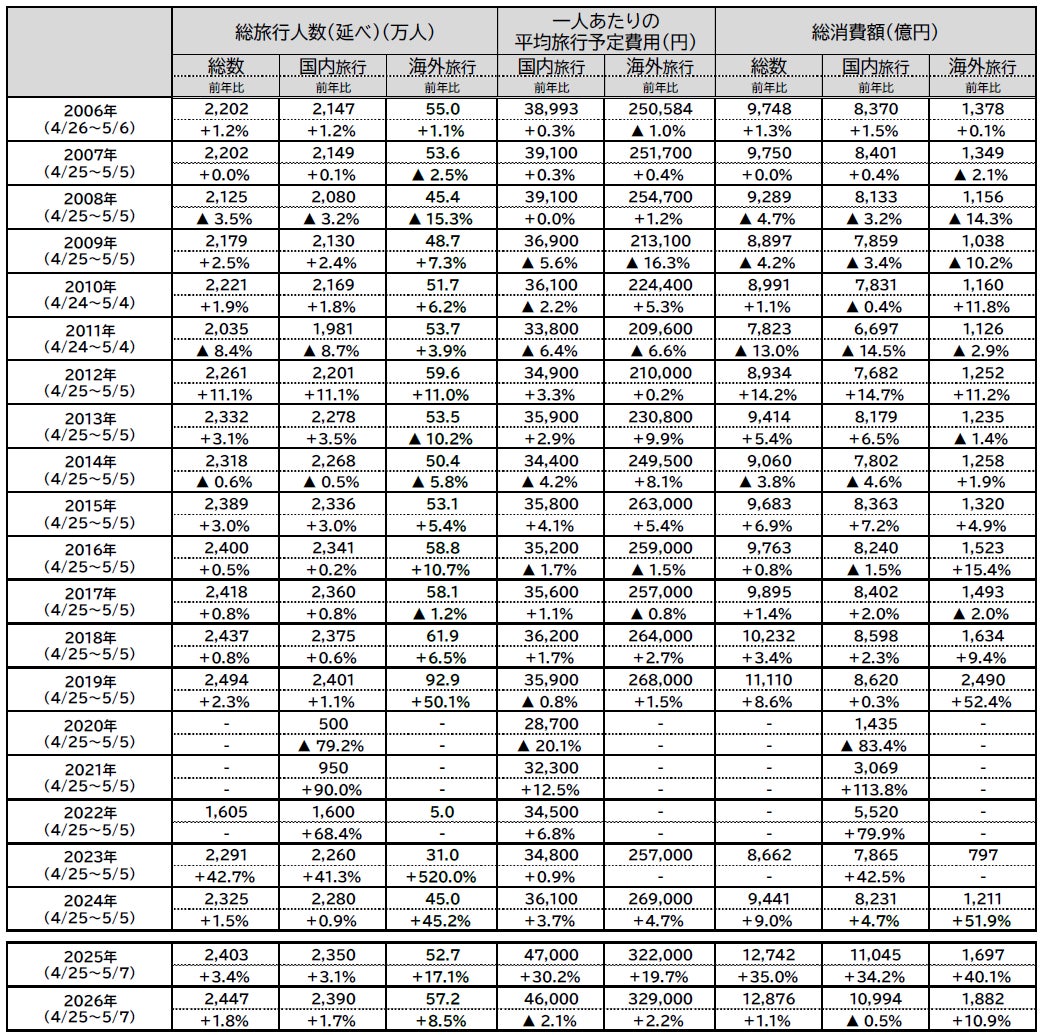

JTB's 2026 Golden Week travel outlook predicts a 1.9% increase in total travelers to 24.47 million, with spending rising slightly to 1.2876 trillion yen. Domestic travel is expected to see a slight increase in travelers and a decrease in average expenditure due to shorter trips, while overseas travel will see more travelers and higher spending, with South Korea, Taiwan, and Southeast Asia being popular destinations. Factors like favorable calendar alignment and a desire for experiences are driving travel intent, though concerns about costs and crowds persist.

📋 Article Processing Timeline

- 📰 Published: April 2, 2026 at 23:00

- 🔍 Collected: April 2, 2026 at 19:38

- 🤖 AI Analyzed: April 18, 2026 at 00:00 (364h 22m after Collected)

JTB has compiled its travel trend outlook for people planning to travel for one night or more during Golden Week (hereafter referred to as GW) from April 25 to May 7, 2026. This report is an estimate based on a survey conducted by the JTB Group, as well as various economic trends, industry trends, transportation and tourism-related data, accommodation booking status, and various opinion surveys. The survey has been conducted continuously since 1969.

Supported by strong travel intent and favorable calendar alignment, the number of travelers is increasing, and the average planned travel expenditure is on par with the previous year.

Domestic travel sees an increase in short durations, nearby destinations, and private car usage, with efforts to enjoy travel while managing costs amidst rising prices.

Overseas travel focuses on 3- to 5-night trips, with South Korea, Taiwan, and Southeast Asia being popular.

● Total Golden Week travelers: 24.47 million (101.9% YoY)

● Total travel spending: 1.2876 trillion yen (101.1% YoY)

● Domestic travel: Travelers 23.90 million (101.7% YoY), Average planned travel expenditure: 46,000 yen (97.9% YoY), Travel spending: 1.0994 trillion yen (99.5% YoY)

● Overseas travel: Travelers 572,000 (108.5% YoY), Average planned travel expenditure: 329,000 yen (102.2% YoY), Travel spending: 188.2 billion yen (110.9% YoY)

【Domestic Travel]

➤ Traveler numbers show a slight increase, supported by favorable calendar alignment and strong travel intent.

➤ Average planned travel expenditure remains high due to factors like rising prices, and shows a slight decrease due to shorter trip durations.

➤ Destinations are mainly nearby, short-term trips within the traveler's region of residence, with an increase in private car usage for short-distance travel.

➤ Travel purposes include "spending time with family," "dining and tasting local flavors," and "relaxing and taking it easy."

【Overseas Travel]

➤ Traveler numbers are increasing, boosted by the recovery of international flights exceeding pre-pandemic levels and favorable calendar alignment.

➤ Average planned travel expenditure shows a slight increase due to longer trip durations and the impact of a weaker yen and rising prices.

➤ Popular destinations include relatively nearby locations such as South Korea, Taiwan, and Southeast Asia, with Europe and North America also showing sustained popularity.

1. This Year's GW Calendar and Travel Trends

The 2026 Golden Week calendar features a 5-day holiday from Saturday, May 2nd to Wednesday, May 6th. Taking Thursday, April 30th and Friday, May 1st off results in an 8-day holiday, and taking Thursday, May 7th and Friday, May 8th off results in a 9-day holiday. Connecting these can lead to a 12-day or longer continuous break, making it a period suitable for taking extended time off, depending on the combination. Here, we asked about travel intentions for the 2026 GW period (April 25 - May 7), including returning home.

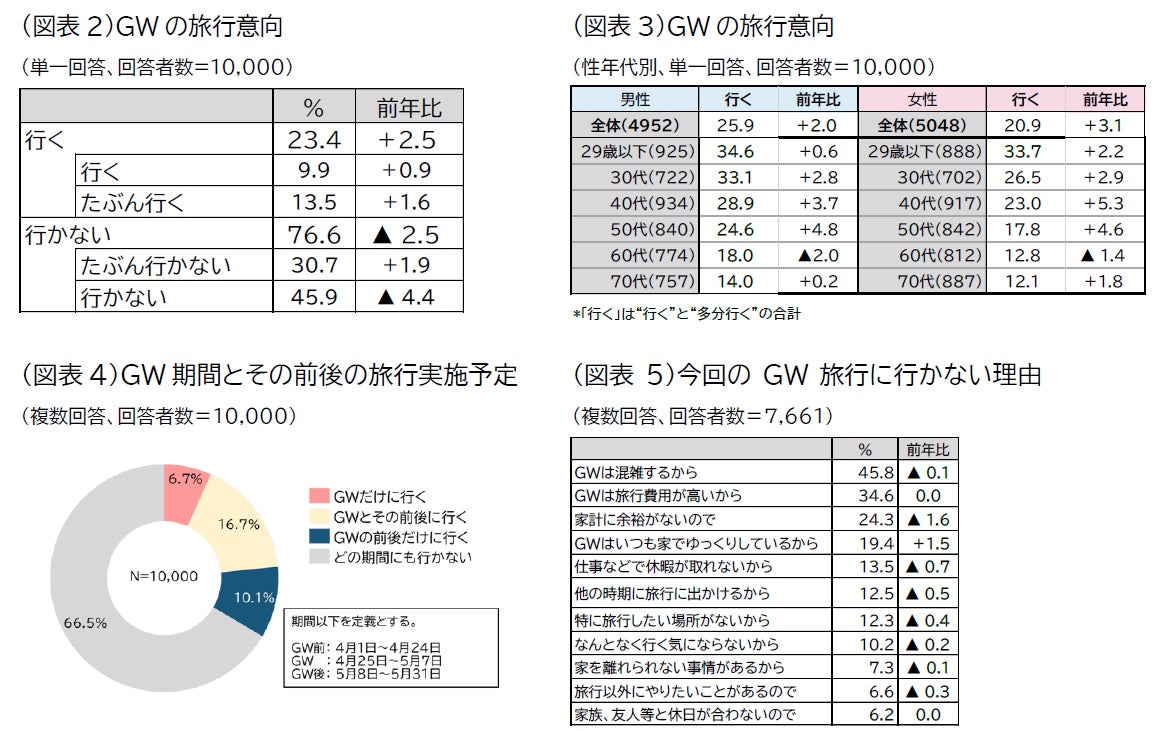

The proportion of respondents who answered "will travel" (total of "will travel" and "probably will travel") during the GW period was 23.4%, an increase of 2.5 percentage points compared to the previous year (April 25 - May 7, 2025) (Figure 2).

By gender and age, the highest rates were for "Male under 29 (34.6%)," "Female under 29 (33.7%)," and "Male in their 30s (33.1%)," all exceeding 30%. Furthermore, travel intent increased year-on-year for all age groups except for males and females in their 60s, with particularly high growth rates observed for both males and females in their 40s and 50s (Figure 3).

When asked about travel before GW (April 1-24) or after GW (May 8-31), "Only during GW" accounted for 6.7%, while "During GW and its surrounding days" accounted for 16.7%, and "Only before/after GW" accounted for 10.1%. The number of people traveling "only before/after GW" exceeded those traveling "only during GW." It is believed that the trend of travel dates being dispersed continues, with more people taking vacation days before or after the long holiday due to increased work flexibility (Figure 4).

Reasons for not traveling included, in order: "GW is crowded (45.8%)," "GW travel costs are high (34.6%)," and "Lack of household budget (24.3%)." Additionally, "I always relax at home during GW (19.4%)" was the only option that increased year-on-year. This suggests that some people choose to spend their holidays without overexerting themselves, considering the crowds and high costs (Figure 5).

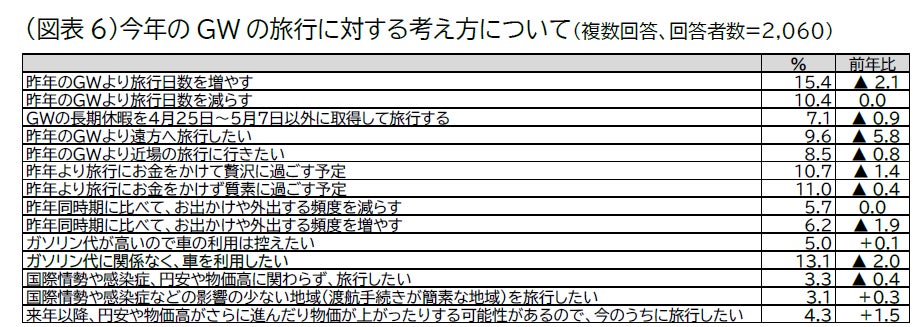

Among the 2,060 respondents planning to travel during GW, we asked about their plans for this year's GW travel. Regarding destinations, "Want to travel further than last year's GW (9.6%)" decreased by 5.8 percentage points compared to last year, significantly exceeding the 0.8 percentage point decrease in "Want to travel to nearby destinations than last year's GW (8.5%)." Also, "Plan to spend extravagantly by spending more money than last year (10.7%)" decreased by 1.4 percentage points, falling below "Plan to spend modestly by spending less money than last year (11.0%)." Furthermore, the proportion of respondents indicating "increase" in duration and frequency of travel shows a downward trend. Regarding gasoline, "Want to use the car regardless of gasoline cost (13.1%)" decreased by 2.0 percentage points.

Additionally, while "Want to travel regardless of international situation, infectious diseases, weak yen, or rising prices (3.3%)" decreased by 0.4 percentage points, "Want to travel to regions with less impact from international situations, infectious diseases, etc. (3.1%)" increased by 0.3 percentage points, and "Since there's a possibility of further escalation of the weak yen and rising prices next year, I want to travel now (4.3%)" increased by 1.5 percentage points. Amidst continuing uncertainty, there are indications of a segment of people who prioritize traveling "when they can" (Figure 6).

2. Domestic Travel Trends

Total domestic travelers are estimated at 23.90 million (101.7% YoY), with an average planned travel expenditure of 46,000 yen (97.9% YoY) and total domestic travel spending of 1.0994 trillion yen (99.5% YoY). Despite the impact of rising prices, travel intent remains robust, supported by favorable calendar alignment, with traveler numbers showing a slight year-on-year increase. While travel costs remain high, a slight decrease is predicted due to shorter travel durations (Figure 1).

We analyzed the travel trends of 1,941 respondents among the 2,060 survey participants who indicated "Japan" as their domestic travel destination for this GW.

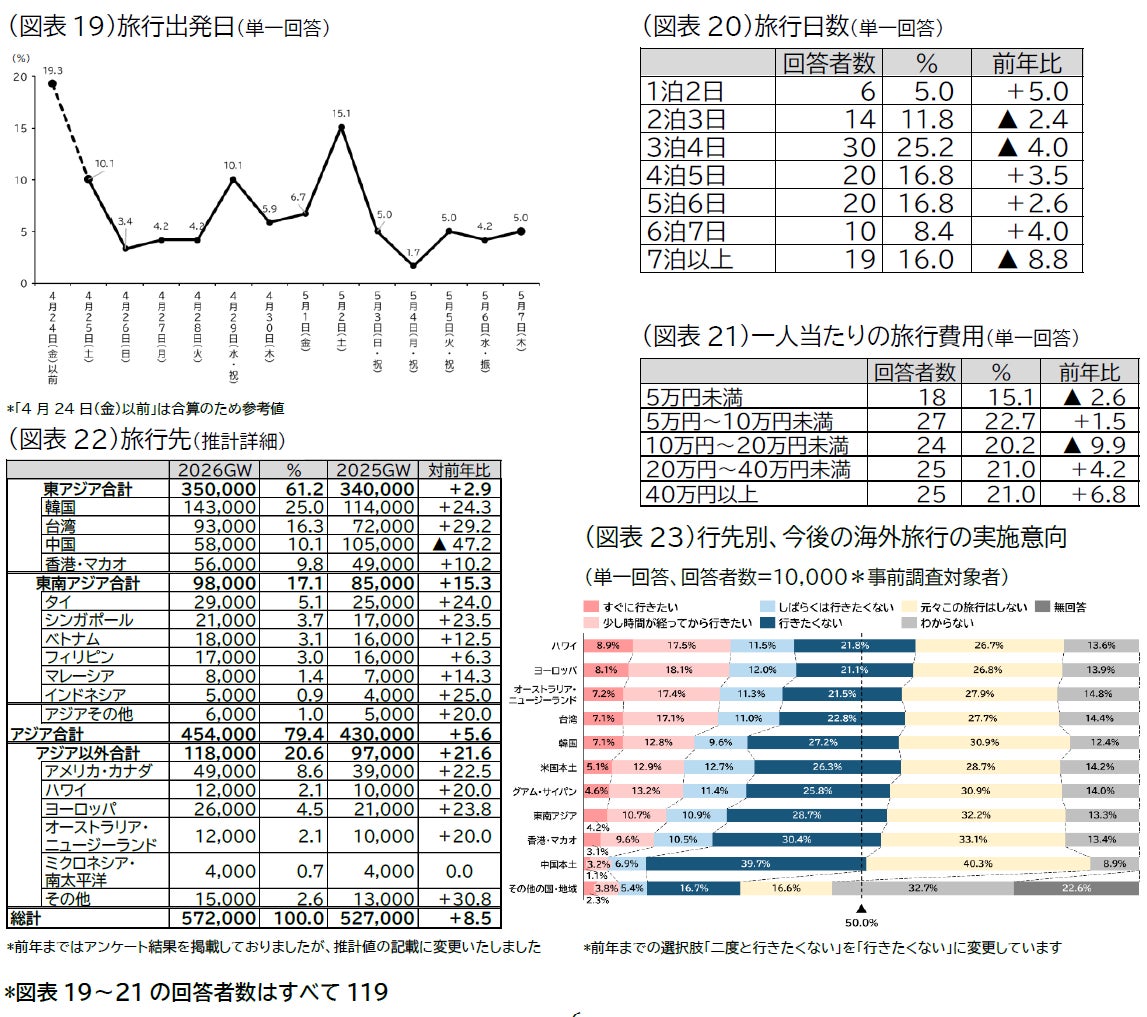

Departure Dates: The peak departure date is "Saturday, May 2nd (19.6%)," followed by "Sunday, May 3rd (Holiday) (14.7%)," and "Before Friday, April 24th (14.5%)." The peak is centered around the latter half of the 5-day holiday, but there's also a significant proportion of early departures before April 24th, suggesting an effort to avoid crowds (Figure 7).

Travel Duration: Overall, "1 night 2 days (39.9%)" was the most common, an increase of 6.4 percentage points from the previous year. Following this, "2 nights 3 days (32.0%)" decreased by 0.7 percentage points, and "3 nights 4 days (16.2%)" decreased by 3.6 percentage points. Durations of 2 nights or more did not increase, showing a total decrease of 6.5 percentage points (Figure 8).

Travel Purpose: The most common purpose is "Spending time with family" at 28.5%. This is followed by "Dining and tasting local flavors (25.9%)" and "Relaxing and taking it easy (24.8%)." This indicates a strengthening trend towards prioritizing the time spent with companions over sightseeing or experiences at the destination (Figure 9).

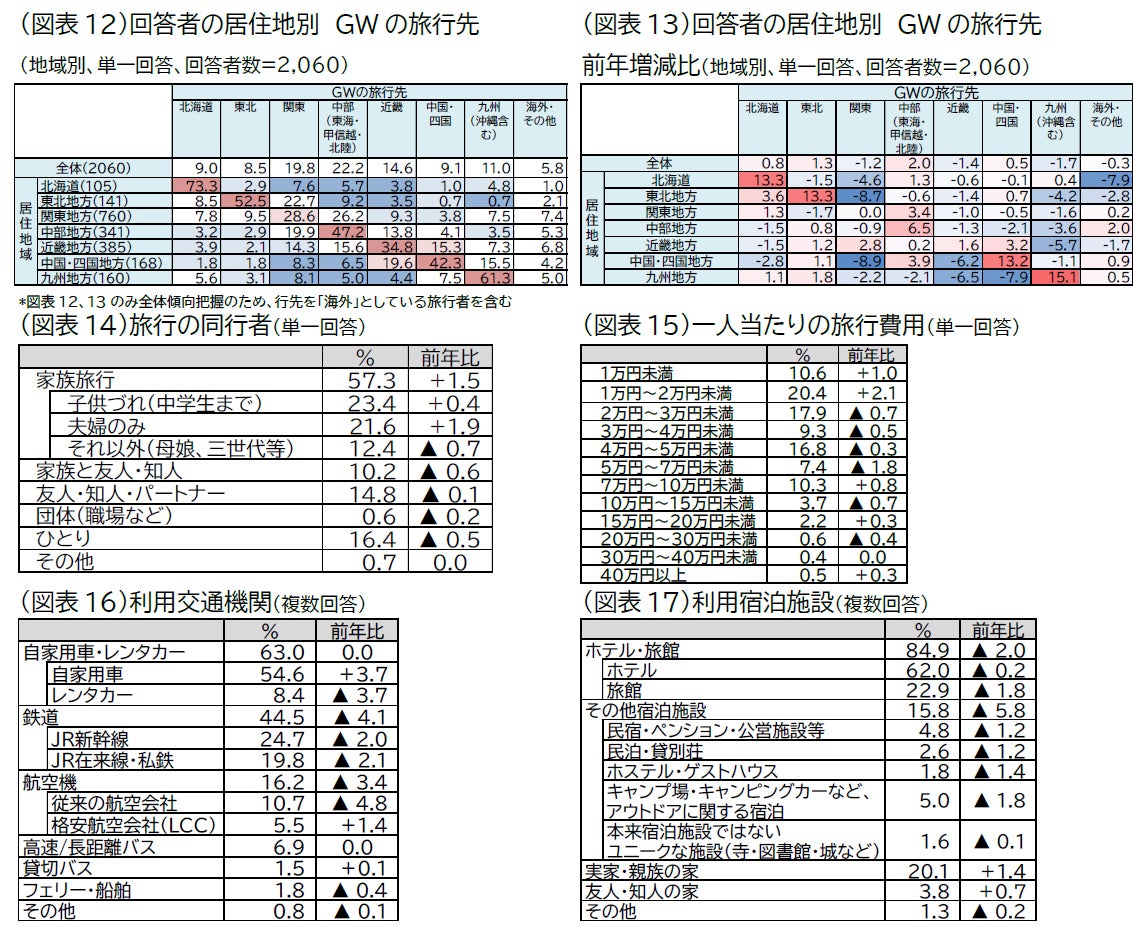

Destinations: "Kanto (21.0%)" was the most popular, but it decreased by 1.4 percentage points from the previous year. "Kinki (15.5%)" also decreased by 1.6 percentage points. In terms of growth rate, "Koshinetsu (8.6%)" increased by 1.8 percentage points, "Tohoku (9.0%)" increased by 1.3 percentage points, and "Tokai (10.8%)" increased by 1.2 percentage points (Figure 10).

The main reasons for choosing these destinations were "Because there are places I want to go (40.4%)," followed by "Because I can go by private car or rental car (18.2%)," and "Because it's my hometown (17.5%)" (Figure 11). Analyzing destinations by region of residence, the proportion of intra-regional travel (where the destination is in the same region as the place of residence) was highest in "Hokkaido" at 73.3%, followed by "Kyushu (61.3%)" and "Tohoku (52.5%)." On the other hand, "Kanto" was the lowest at 28.6% (Figure 12). Compared to the previous year, the proportion of intra-regional travel increased in all regions except Kanto. Last year, all regions except Kinki (which hosted the 2025 Osaka-Kansai Expo) saw a decrease, indicating a stronger intra-regional travel trend this year (Figure 13).

Companions: "Family trip with children (up to junior high school) (23.4%)" was the most common, an increase of 0.4 percentage points from the previous year, followed by "Couple only (21.6%)," which increased by 1.9 percentage points. Family trips in total increased by 1.5 percentage points, while all other categories decreased (Figure 14).

Average Planned Travel Expenditure per Person: "10,000 to less than 20,000 yen (20.4%)" was the most frequent, an increase of 2.1 percentage points from the previous year. Following this were "20,000 to less than 30,000 yen (17.9%)" and "40,000 to less than 50,000 yen (16.8%)," but all of these decreased from the previous year. The increase in the 20,000 yen and under category suggests a stronger trend towards cost-saving in travel expenses (Figure 15).

Transportation Used: "Private car (54.6%)" was the most used, followed by "JR Shinkansen (24.7%)" and "JR local lines/private railways (19.8%)." While "JR Shinkansen" and "JR local lines/private railways" decreased, "Private car" increased by 3.7 percentage points and "Low-cost carriers (LCC) (5.5%)" increased by 1.4 percentage points. "Highway/long-distance buses" and "charter buses" remained at similar levels to the previous year, indicating a tendency to choose transportation methods that reduce costs (Figure 16).

Accommodation Used: "Hotels (62.0%)" were the most common, followed by "Ryokan (traditional inns) (22.9%)," but both decreased. Compared to the previous year, all accommodation types decreased, while "Parents' or relatives' homes (20.1%)" increased by 1.4 percentage points and "Friends' or acquaintances' homes (3.8%)" increased by 0.7 percentage points (Figure 17).

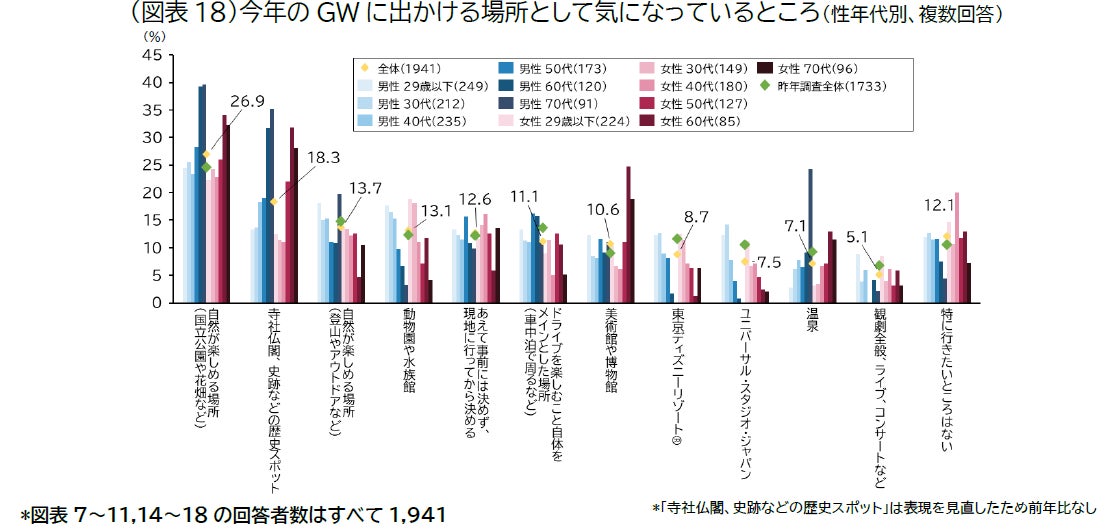

Places of Interest: "Places where nature can be enjoyed (national parks, flower fields, etc.) (26.9%)" was the most popular, followed by "Historical spots such as temples, shrines, and historic sites (18.3%)," and "Places for outdoor activities like hiking and other nature enjoyment (13.7%)" (Figure 18).

JTB's popular domestic travel destinations include theme parks such as Tokyo Disney Resort® (including Tokyo) and Universal Studios Japan (including Kansai). Long-distance destinations requiring JR or air travel, such as Kyushu and Okinawa, are also performing well.

3. Overseas Travel Trends

We estimate the number of overseas travelers at 572,000 (108.5% YoY). Driven by the strong inbound tourism market, international flight capacity has exceeded pre-pandemic levels. Coupled with favorable calendar alignment and increased travel intent, numbers are expected to surpass last year's. Average planned travel expenditure is 329,000 yen (102.2% YoY), and total overseas travel spending is 188.2 billion yen (110.9% YoY). Specific trends are described below.

Among the 2,060 survey respondents, 119 people (5.8%) indicated "Overseas" as their GW travel destination this year. The peak departure dates are "Before Friday, April 24th (19.3%)," followed by "Saturday, May 2nd (15.1%)," with "Saturday, April 25th (10.1%)" and "Wednesday, April 29th (Holiday) (10.1%)" tied. The most common travel duration is "3 nights 4 days (25.2%)," a decrease of 4.0 percentage points from the previous year, followed by "4 nights 5 days (16.8%)," which increased by 3.5 percentage points, and "5 nights 6 days (16.8%)," which also increased by 2.6 percentage points. Compared to the previous year, 4- to 6-night trips have also increased, possibly due to the ease of taking extended holidays. Conversely, "1 night (5.0%)" has increased by 5 percentage points, whereas it was 0 last year. Regarding travel costs, "50,000 to less than 100,000 yen (22.7%)" was the most common, an increase of 1.5 percentage points from the previous year, followed by "200,000 to less than 400,000 yen (21.0%)" which increased by 4.2 percentage points, and "400,000 yen or more (21.0%)" which increased by 6.8 percentage points (Figure 21).

Destinations were estimated by country/region. The top destinations were "South Korea (25.0%)," followed by "Taiwan (16.3%)." Southeast Asia as a whole accounted for 17.5%, and Asia as a whole accounted for 79.0%. On the other hand, growth rates show double-digit increases for longer-haul destinations such as "USA/Canada (North America)," "Europe," and "Australia/New Zealand," indicating sustained popularity (Figure 22).

JTB's popular overseas travel destinations include Hawaii, Taiwan, South Korea, Guam, as well as the US West Coast, Australia, and France.

When asked about future overseas travel intentions among all survey respondents, including those not traveling this GW, "Hawaii (8.9%)" had the highest "Want to go soon" response, followed by "Europe (8.1%)" and "Australia/New Zealand (7.2%)" (Figure 23).

4. Economic Environment and Consumer Sentiment Surrounding Travel and Leisure Consumption

While the Japanese economy continues a gradual recovery, risks stemming from external factors remain significant, such as rising oil prices due to tensions in the Middle East and uncertainty surrounding US trade policy, making the outlook uncertain. The Nikkei Stock Average reached a temporary high of over 58,000 yen in February 2026, but fluctuated around 52,000 yen in March, indicating market instability.

The government's monthly economic report stated in its February 2026 assessment that "The economy is gradually recovering, although the impact of US trade policy remains." Personal consumption has also continued to show "signs of picking up" since the judgment in September 2025. However, concerns such as the risk of price increases due to the Middle East situation and US policy trends mean that the recovery trend cannot be viewed with excessive optimism.

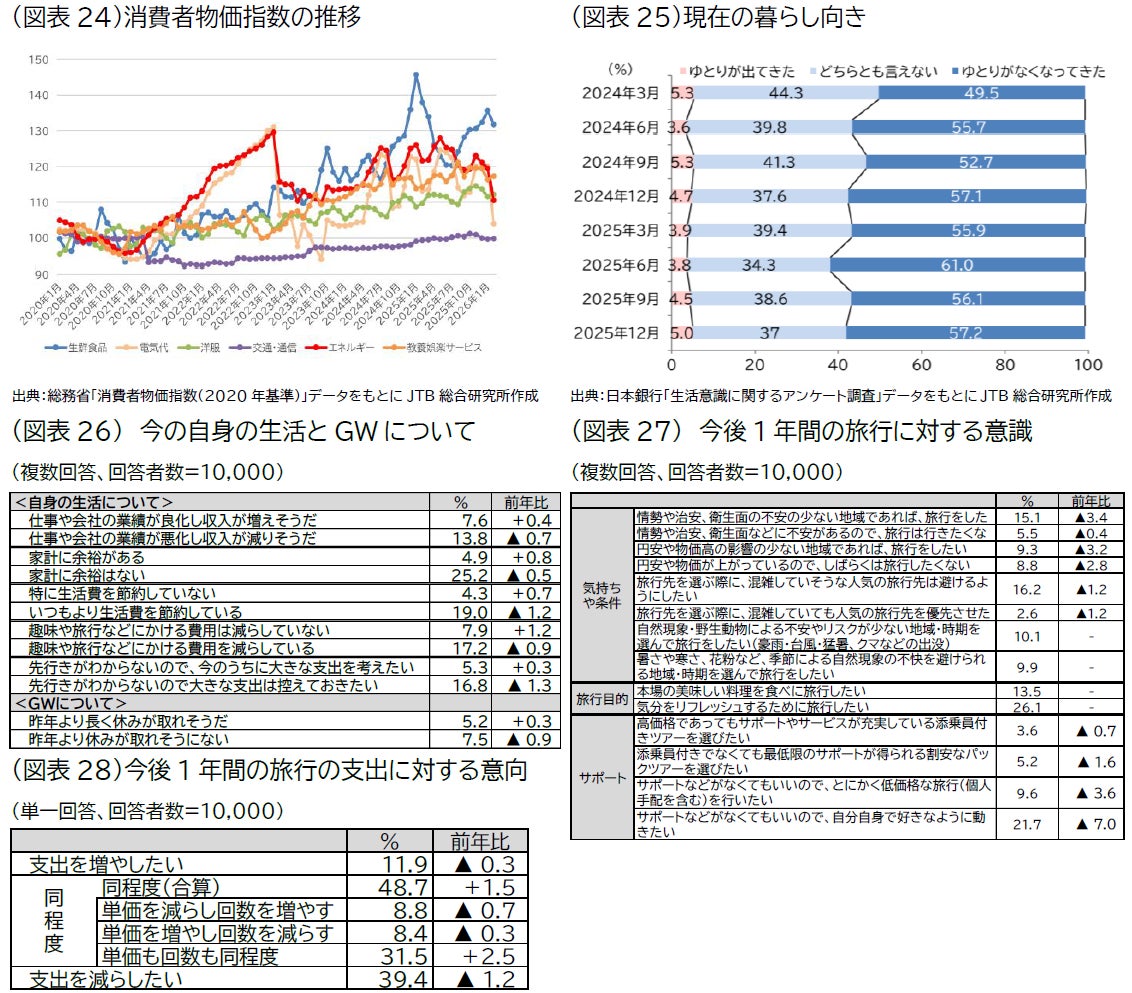

Regarding price trends, in the January 2026 Consumer Price Index, "fresh food" continued to rise, while "energy," "electricity bills," and "clothing" have passed their peak from the previous year, with the pace of increase moderating. In terms of wages and consumption, while real wages were negative year-on-year for the full year in 2025, the preliminary figure for January 2026 was 1.3%, showing a positive turn and signs of improvement. The Bank of Japan's "Survey on Living Consciousness" also shows an increasing trend in "feeling more comfortable" since June 2025 (Figure 25).

Current Living Situation and GW Holiday Plans

According to a survey conducted by JTB, responses regarding current personal finances and GW plans showed an increase in "My work and company performance are improving, so income is likely to increase (7.6%)" and "My household budget has some room (4.9%)" compared to the previous year. Additionally, "I am not particularly saving on living expenses (4.3%)," "I have not reduced spending on hobbies or travel (7.9%)," and "Since the future is uncertain, I want to make major expenditures now (5.3%)" also increased. This suggests a shift from the saving trend of previous years to a more consumption-oriented mindset. Despite rising prices, more people are likely to enjoy travel while finding ways to manage costs. The favorable calendar alignment also contributed to an increase in "It seems I can take a longer break than last year (5.2%)," a 0.3 percentage point increase, and a decrease in "It seems I cannot take as long a break as last year (7.5%)," a 0.9 percentage point decrease. This ease of taking time off is thought to contribute to the increase in overseas travel (Figure 26).

Regarding consciousness towards travel in the coming year, "I want to travel if it's to regions with less anxiety regarding the situation, public safety, and hygiene (15.1%)" decreased by 3.4 percentage points from the previous year, but it still surpasses "I don't want to travel due to anxiety about the situation, public safety, and hygiene (5.5%)." Furthermore, "I want to travel to regions less affected by the weak yen and rising prices (9.3%)" and "Since the yen is weak and prices are rising, I don't want to travel for a while (8.8%)" were close, indicating that a certain number of people are not concerned about price and exchange rate impacts. There is also a desire to choose travel destinations that are safer and more comfortable, considering natural phenomena and wildlife, such as "I want to travel to regions/times with fewer anxieties and risks from natural phenomena/wildlife (10.1%)" and "I want to travel to regions/times that avoid the discomfort of seasonal natural phenomena like heat, cold, or pollen (9.9%)" (Figure 27).

Regarding "Intentions for travel expenditure in the coming year," "About the same (combined, 48.7%)" increased by 1.5 percentage points from the previous year, with "Same unit price and same number of times (31.5%)" increasing by 2.5 percentage points within this category. "Want to increase spending (11.9%)" decreased by 0.3 percentage points, and "Want to decrease spending (39.4%)" decreased by 1.2 percentage points. Overall, it appears that people are planning to travel while maintaining a similar budget (Figure 28).

Keywords of Interest for Travel

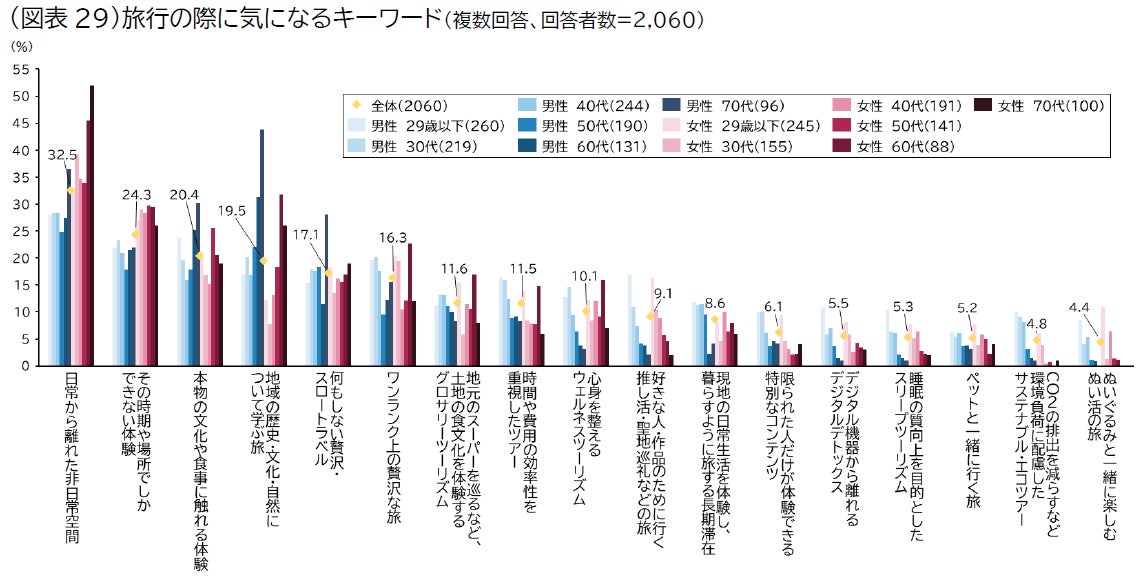

Finally, when asked about keywords of interest for travel to those who planned to travel this GW, "Non-everyday, extraordinary space away from daily life (32.5%)" was the most common, followed by "Experiences that can only be had at that time and place (24.3%)," and "Experiences of authentic culture and food (20.4%)." By gender and age, "Learning about regional history, culture, and nature" was high among males and females in their 60s and 70s. Among males and females under 29, keywords related to hobbies, self-recovery, and social media affinity, such as "Oshi-katsu (fan activities) and pilgrimage to sacred sites for favorite people/works," "digital detox away from digital devices," "sleep tourism aimed at improving sleep quality," and "Nuigurumi-katsu (plush toy activities) trips to enjoy with stuffed animals," ranked high. The values sought in travel vary by generation, and it seems that travel is expanding beyond traditional tourism to encompass experiences that cater to people's diverse interests (Figure 29).

(Figure 30) "Estimated figures for GW travel numbers and spending" trend

* The target period has been changed to April 25 - May 7 from the 2025 fiscal year.

* Survey started in 1969. Overseas travel numbers are actual figures until 2025 (2026 is an estimate). Domestic travel numbers are estimates, and some revisions have been made to the previous year's announced figures based on trend results.

* Average planned travel expenditure has been estimated since 1999. Some revisions have been made to the previous year's announced figures based on trend results.

* Market research has been changed to an internet survey since 2019.

* In 2020 and 2021, average overseas travel expenditure and overseas travel consumption were calculated.

* Total consumption for 2021-2023 cannot be directly compared, so year-on-year changes are not indicated.

[Golden Week Travel Trends Survey Methodology]

Survey Period: March 6 - 11, 2026

Target: Individuals aged 15 to 79 nationwide

Sample Size: Preliminary survey 10,000 people, Main survey 2,060 people

(The main survey was conducted by selecting individuals who responded "GW will travel / probably will travel" during the preliminary GW survey)

Survey Content: Travel for one night or more scheduled for April 25 - May 7, 2026

(Domestic travel limited to sightseeing and returning home; overseas travel includes business trips)

Survey Method: Internet survey

※ Due to rounding, there may be discrepancies in subtotals and differences from previously published survey results.